Carbon Neutrality on Sale

Finding the cheapest cap and trade market to “offset emissions” is just political arbitrage.

Companies these days are finding new and creative ways to go “carbon neutral”. For a while, they were buying carbon offsets, but those got a bad name, because some of them are flimflam, uh, I mean, not really additional. One of the newer trends is to buy, and then retire, allowances from cap and trade markets. The argument is that 1 metric tonne of CO2 allowances retired is 1 tonne that will never be emitted.

(Source)

If you are a regular reader of this blog, you know Jim Bushnell has countered that assertion with his compelling slogan, and future epitaph, “The cap is not really a cap.” (TCINRAC, soon to be available on bumper stickers, T-shirts and baseball caps.) In other words, most cap and trade programs have explicit price ceilings and floors at which the cap is flexible. At the floor price, the cap quantity is reduced in order to maintain that price. And at the ceiling it is expanded. So, the program effectively turns into a tax. And when you pay a pollution tax, it doesn’t reduce someone else’s emissions.

I fully agree with Jim, and have muttered TCINRAC on occasion myself. Today I want to make a different, but related, point.

(Created with Google Bard)

—

Let’s start by agreeing on one thing about cap and trade markets: if you create more allowances, the price for them will be lower.

Okay, let’s agree on a second thing: the emissions caps in the various CO2 cap and trade programs around the world have been set through negotiation over what is politically, logistically, and economically “feasible”, which has varied across countries and over time.

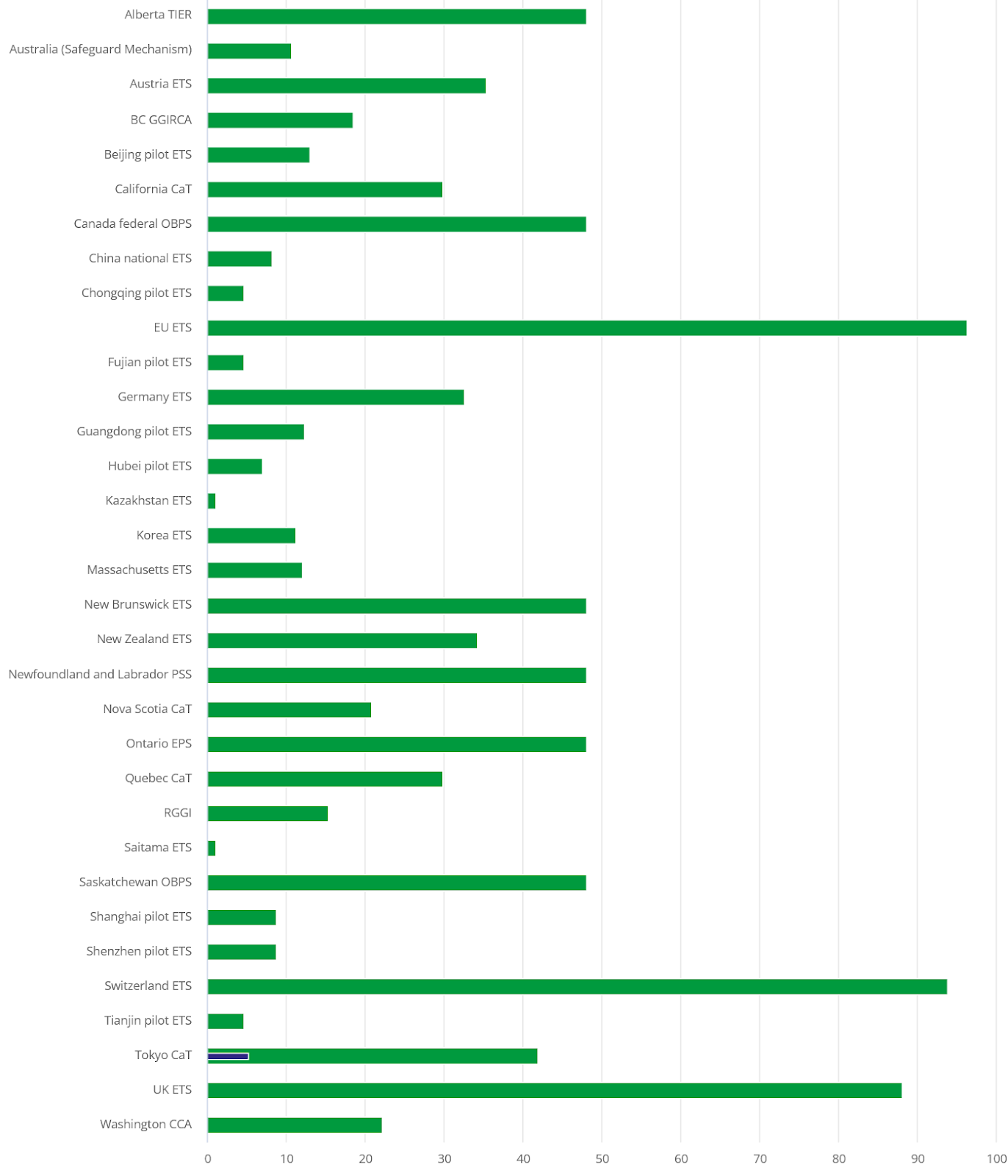

So it really isn’t a surprise that the prices in these markets vary drastically, from the single digits ($US) per metric tonne to nearly the triple digits, even though they are all pricing emissions of the same gas, which has the same environmental effect regardless of where the emissions occur. Thus, a company emitting 1 tonne of CO2 in France currently pays more than 4 times the cost of that same behavior by a company located in Pennsylvania. Yet, both say that they have paid the cost of their pollution, so can count themselves as responsible corporate citizens.

(Source) Carbon trading prices covered by Emission Trading Systems (ETS) worldwide as of March 31, 2023, by jurisdiction (in U.S. dollars per metric tonne of CO2 equivalent)

Obviously, they can’t both be right. In fact, they are both almost certainly wrong. The price in a cap and trade market is not the result of calculating the true cost of the pollution, but rather the result of political/administrative decisions about the level of the emissions cap, as well as the floor and ceiling prices enforced in the market.

Now put on your Captain of Industry hat (or virtual reality headset) and imagine that the company you run wants to go carbon neutral. One of your clever senior vice presidents tells you the firm can do that by buying and retiring cap and trade allowances, thereby reducing the emissions in that market and offsetting the emissions from your company.

Any corporate titan worth their eight-figure salary will quickly realize that the most “cost-effective” way to go carbon neutral is to buy allowances from the cheapest cap and trade market they can find, paying something closer to $10 than $100 per tonne.

Is that a bad thing? After all, they are all the same emissions. Isn’t buying the cheap allowances going to reduce emissions just as much as buying the expensive ones?

Well…No. First of all, TCINRAC.

“Hold on,” Captain of Industry might respond, “we don’t buy allowances that are at the price floor, so we don’t have that problem.”

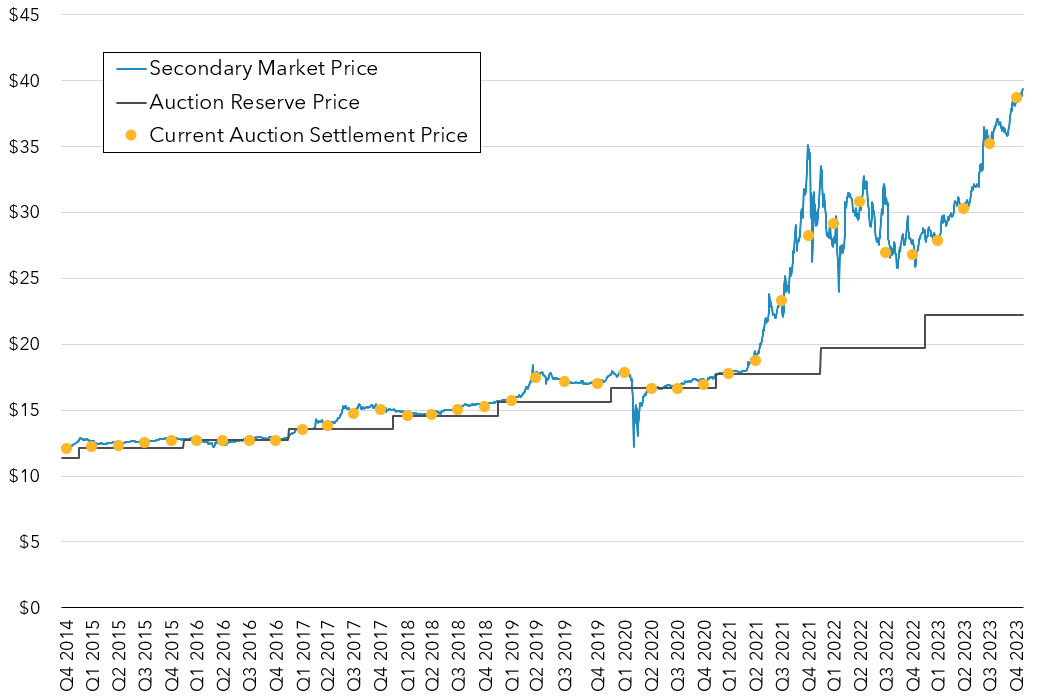

(Source) California Carbon Allowance Prices versus the Auction Reserve Price (price floor)

Well of course you don’t. Prices are seldom exactly at the price floor. But the short history of CO2 allowances suggests they are frequently close. Like most financial instruments, the current value is a probability-weighted average of possible future values. When California’s allowances sat within a dollar of the price floor for many years, the market was saying there was a darn good chance that the administrative mechanism for enforcing the floor would be activated, and California would reduce the supply of allowances (as it eventually did). So, the tonne that Captain’s firm retires quite probably is just displacing a tonne that the state would have removed from the market.

“But wait,” Captain replies, “we buy allowances in markets that don’t have price floors, so our retired CO2 would not have been soaked up by a floor price mechanism.” Not quite, Captain. There’s a natural price floor at zero (and, by the way, quite an attractive price for firms to “neutralize” their emissions). Our own analysis of the macroeconomic and technology uncertainty in allowance demand suggests that zero would not be an implausible outcome for a market that runs for many years.

More importantly, before the price gets to zero, history teaches us that governments are likely to intervene on an ad hoc basis. Since 2013, both the Northeast’s Regional Greenhouse Gas Initiative and the EU’s Emission Trading System changed their rules in response to very low prices, effectively implementing a new price floor. And many observers expect California to lower its emissions cap in the near future, a change that is clearly more likely to occur if the allowance price is low than if it is high.

Sure, there is a theoretical model of cap and trade markets in which buying and retiring a one-tonne allowance reduces total emissions by one tonne. But in the real markets that politically-driven governments establish, cap and trade looks more like an adjustable tax mechanism, not an emissions cap that is forever fixed.

I wouldn’t think much of a company that finds a country with a $10 per tonne tax and goes “carbon neutral” by paying for its emissions there. Why would I think much more of one that “offsets” its emissions by purchasing allowances in a cheap cap and trade market?

—

I am posting frequently these days on Bluesky @severinborenstein

Follow us on Bluesky and LinkedIn, as well as subscribe to our email list to keep up with future content and announcements.

Suggested citation: Borenstein, Severin. “Carbon Neutrality on Sale” Energy Institute Blog, UC Berkeley, January 29, 2024, https://energyathaas.wordpress.com/2024/01/29/carbon-neutrality-on-sale/

Categories

Severin Borenstein View All

Severin Borenstein is Professor of the Graduate School in the Economic Analysis and Policy Group at the Haas School of Business and Faculty Director of the Energy Institute at Haas. He received his A.B. from U.C. Berkeley and Ph.D. in Economics from M.I.T. His research focuses on the economics of renewable energy, economic policies for reducing greenhouse gases, and alternative models of retail electricity pricing. Borenstein is also a research associate of the National Bureau of Economic Research in Cambridge, MA. He served on the Board of Governors of the California Power Exchange from 1997 to 2003. During 1999-2000, he was a member of the California Attorney General's Gasoline Price Task Force. In 2012-13, he served on the Emissions Market Assessment Committee, which advised the California Air Resources Board on the operation of California’s Cap and Trade market for greenhouse gases. In 2014, he was appointed to the California Energy Commission’s Petroleum Market Advisory Committee, which he chaired from 2015 until the Committee was dissolved in 2017. From 2015-2020, he served on the Advisory Council of the Bay Area Air Quality Management District. Since 2019, he has been a member of the Governing Board of the California Independent System Operator.

Would prohibiting third party traders helps control this problem? I realize there’s a liquidity argument, but if third parties essentially change the market they are doing more than just providing liquidity.

As Severin notes, “in the real markets that politically-driven governments establish, cap and trade looks more like an adjustable tax mechanism, not an emissions cap that is forever fixed.”

That is true, and I don’t necessarily think that is a bad thing. “Politcally-driven governments” — that is, all governments of jurisdictions large enough to establish a cap-and-trade program — have macroeconomic responsibilities that generally require regulatory flexibility to be adequately addressed. That’s not the most efficient approach to achieve an optimal program outcome, but “politically-driven” policies don’t operate in a vacuum. In Government, we’re trying to acheive some semblance of socio-economic equilibrium (and equity). In more common parlance, we don’t want the “perfect” (or optimal) policy to be the enemy of the good when it throws that equlilibrium (too far) off balance. I think TCRINRAC works in that context — and I will be happy to purchase a TCRNRAC cap as soon as they are available. But not a bumpersticker. I don’t want any broken windows on my vehicle.

Bravo, Severin (and Jim) – a pet peeve of my own. A possible followup: Renewable Energy Credits (RECs), which inherently double-count clean generation. In a 2007 filing, the Federal Trade Commission wrote:

“In general, carbon offsets are credits or certificates that represent the right to claim responsibility for greenhouse gas emission reductions…In some cases, carbon offset sellers use the proceeds to purchase Renewable Energy Credits (RECs). By acquiring these greenhouse gas reduction credits, purchasers, including individuals and businesses, seek to reduce their “carbon footprints” or to make themselves “carbon neutral.”

“Generators sell their electricity at market prices applicable to conventionally-produced [GHG-emitting] power. Generators then charge for the electricity’s renewable attribute separately by selling certificates to individuals and business purchasers across the country who use them to characterize the conventional electricity they buy as renewable.

“The FTC has an important role to play in combating unfair and deceptive practices in this market…but even if a consumer could verify a project’s existence, it likely would be impossible for the average consumer to determine whether the scientifically complex project actually reduces atmospheric carbon in the amount claimed, or how much the consumer’s offset purchase actually contributes to the project.”

Here the FTC is mistaken. Determining whether a REC reduces atmospheric carbon for the amount claimed is not “scientifically complex” at all – it’s trivial arithmetic:

GHG emissions produced by a solar farm that generates 1 megawatthour (MWh) of clean electricity: 0 lbs.

GHG emissions produced by a U.S. gas plant that generates 1 MWh of clean electricity: 970 lbs. (average)

Solar farm sells 1-MWh REC to gas plant, both take credit for associated “clean energy attributes.” Total energy generated = 2 MWh; total emissions = 970 lbs. Who takes responsibility for 970 lbs. of CO2 emitted into the atmosphere? No one.

Obviously, a ton of CO2 here or there is not going to make a difference. When 27 states have Renewable Portfolio Standards, however, and all of their fossil plants are now generating “clean” electricity, it’s another story.

My epitaph: The REC Is Not Really Renewable (TRINRR).

https://www.federalregister.gov/documents/2007/11/27/E7-23006/guides-for-the-use-of-environmental-marketing-claims-carbon-offsets-and-renewable-energy

“Solar farm sells 1-MWh REC to gas plant, both take credit for associated “clean energy attributes.””

That’s incorrect. The solar farm gave up its clean energy credit to the owner of the gas plant (or the purchaser of the gas plant output) and the solar farm output is no longer counted towards the RPS, for example. There is no double counting in this case.

I’m glad you made this comment. I agree, there is no double counting. And to be specific, the REC is sold to a retail energy provider who uses it for state RPS compliance. That retail energy provider may own or otherwise procure its wholesale power from a gas plant, but the REC is technically part of the retail seller’s RPS compliance for its retail sales.

As for the original comment about a 2007 FTC filing, I’ll note that there has always been a legitimate interest in avoiding double counting and other misrepresentations in these various carbon mitigation rules, and back then the FTC may have very well uncovered a problem that needed fixing. But these systems are continuously being tinkered with to avoid gaming.

One issue relating to “additionality” that is seldom discussed in the popular media is the “waterbed effect”, whereby cap-and-trade operates to nullify the environmental benefit of all additional climate actions in capped sectors.

For example, see LAO’s 2016 report re the GGRF:

“Spending on Capped Sources Likely Has No Net Effect on Overall Emissions.”

https://lao.ca.gov/reports/2016/3328/cap-trade-revenues-012116.pdf#page=14

See also the 2022 IEMAC report re the nullifying effect of C&T on the IRA:

“Mitigating ‘waterbed’ effects: … If the allowance price remains above the price floor, this shift in allowance use will displace emissions reductions that were induced by federal IRA incentives. …”

https://calepa.ca.gov/wp-content/uploads/sites/6/2023/02/2022-ANNUAL-REPORT-OF-THE-INDEPENDENT-EMISSIONS-MARKET-ADVISORY-COMMITTEE-2.pdf#page=19

C&T similarly nullifies the impact of local Climate Action Plans in capped sectors. CAP administrators are generally oblivious to this effect; see St-Louis and Millard-Ball, 2016:

“… the limitation of cap-and-trade on the city’s ability to reduce aggregate emissions is not addressed in any of the 72 Californian [climate action] plans reviewed …”

https://doi.org/10.1177/0263774X16636117

If the supply of allowances is determined by the cap, then the purchase and retirement of allowances yields additional emission reductions in capped sectors; all other actions do not. If the supply is controlled by a predetermined allowance price (e.g. the floor or ceiling in C&T), then the situation is reversed: Allowance purchase and retirement won’t affect emissions because the allowance supply is marginally unlimited, whereas paying for emission reductions over the regulated price will be additional.

The more fundamental issue for C&T, which I’ve not seen addressed in any of these Haas Institute blogs, is what criteria should determine the C&T price floor and ceiling levels and whether there is any good policy rationale for setting the floor at a level any lower than the ceiling. Also, how should the money from carbon pricing be spent?

If all firms faced a true carbon cap everywhere and they could move their production among different regions/locations, I don’t see how how buying credits in the cheapest CTP market is inherently a problem. It’s just an example of gains from trade. It seems the real story here is that large firms do not face GHG controls everywhere and going carbon neutral is more about appearance than compliance. Whether and how a CTP allows offsets from other CTPs seems to be part of the answer here.

I’d buy a TCINRAC baseball cap!

Me too! But I’m wondering if it’s going to be a cap that’s not really a cap.