What Does Capital Really Cost a Utility?

A new study suggests excess compensation to shareholders is costing ratepayers billions.

Regulating an electric or gas utility is a tough job. You want utilities to have the funding they need to serve the public reliably and safely while also keeping rates under control and distributing the revenue burden fairly among customers. Setting rates and monitoring the service performance of utilities gets a lot of attention. What gets much less attention is one of the biggest challenges the regulator faces: figuring out a utility’s costs.

For many costs this seems trivial – the regulator can see what the company paid for everything from fuel to software to the CEO simply by looking at the utility’s books. There is, of course, still the question of whether the utility is overpaying or is using too much (or too little) of an input.

But when it comes to the cost of capital things get murkier. Determining the interest rate the utility must pay lenders or the rate of return it must pay shareholders when they finance investment by issuing stock has been a constant challenge since utility regulation began about a century ago. Unlike most other inputs to utility operations, the cost of capital depends very much on the utility itself, in particular on its finances and risk.

A regulator can see the interest rate the utility pays to a lender or bond purchaser, though there is always concern that the utility isn’t getting the best deal it could in those thin markets. The much bigger problem, however, is how much to compensate shareholders who own a piece of the firm. Those costs don’t appear anywhere on the books and are not straightforward to estimate.

These numbers really matter. US investor-owned electric utilities had assets of nearly $1.4 trillion when 2022 started, and about half of that is financed with shareholder equity. That’s why a lot of time in utility rate cases is spent fighting over the relatively obscure technical question of how much return investors require in order to buy the utility’s stock.

A new Energy Institute working paper by recently-graduated EI alumni, Karl Dunkle Werner and Stephen Jarvis, takes a deep dive into this question and suggests that U.S. regulators are not doing a great job overseeing these costs.

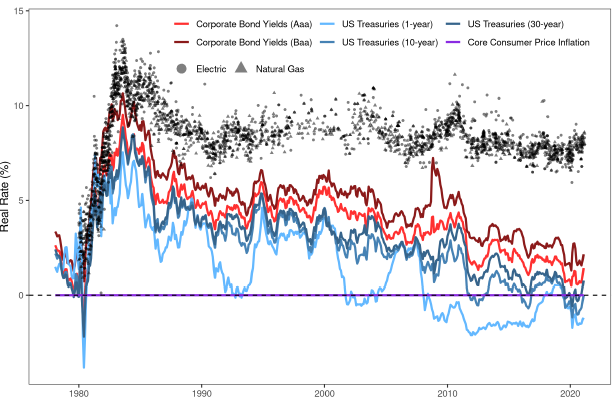

Karl and Stephen (K&S) do this by collecting data on over 3500 regulatory rate cases for electricity and natural gas utilities between 1980 and 2021. They then compare the allowed rate of return on equity to a variety of capital cost indexes, including government and corporate bonds. As the figure below shows, the real (inflation-adjusted) return regulators allow equity investors to earn has been pretty steady over the last 40 years, while many different measures of the actual cost of capital have been declining.

These trends could be explained if utilities have gotten riskier over the last 40 years. But if that were the case it would affect bond ratings, as well as the cost of equity. Increased industry risk would be borne more by equity than debtholders, but it would still be hard to explain a substantial change in the riskiness of utility equity while their debt remained rock-solid. As the paper shows, utility debt ratings have barely budged. That may be a surprise to some folks in California – it’s easy to think of particular utilities that may face more risk today than in past decades – but overall the folks who rate the riskiness of US utilities’ don’t see a systematic trend in recent decades.

All these different benchmarks yield different estimates of the gap in allowed equity returns compared to 25 years ago, but the median is around 2 percentage points, which is real money when it is multiplied by about $700 billion in equity financing of electric utilities alone. Still, there is a valid question of whether utilities are being over-compensated today or were being under-compensated 25 years ago.

But K&S don’t just compare to debt ratings. They also look at the direct economic models of what equity should actually cost, built around what’s known as the Capital Asset Pricing Model (CAPM), the workhorse finance model for asset valuation that is frequently referenced in regulatory hearings. This approach accounts for how risky a company is and the market compensation for taking on extra risk. Consistent with earlier research on utility equity returns, they find that there is also a significant and growing gap between the return regulators allow shareholders and what the CAPM would say they need to be paid to attract investment. They also show just how sensitive this approach is to the underlying assumptions, a fact that utilities are no doubt aware of and that should make regulators wary.

Along the way, the study finds an interesting empirical pattern that suggests what might be going on with these regulatory decisions. Both the return on equity requested by utilities and the return granted by regulators respond more quickly to rises in market measures of capital cost than to declines. In other words, utilities get in there quickly and demand higher returns when they can make the case shareholders are being under-compensated, and regulators respond to those demands. But when shareholders are being over-compensated, the adjustment tends to take longer (consistent with research that Paul Joskow did nearly 50 years ago), about twice as long, K&S estimate. Combining this slow response to over-compensation with the declining cost of capital over most of the last four decades (at least until 2022 came along) would explain why the gap in equity returns has widened on average.

We worry about regulators over-compensating shareholders because the costs are paid through higher utility rates, which disproportionately hurt the poor, as Jim Sallee blogged about last week. And higher electric rates undermine building and transportation decarbonization

But utilities also have an incentive to overinvest in capital projects if they are earning an outsized return on those investments. Sure enough, the paper finds that every extra percentage point of allowed return on equity causes a utility’s capital rate base to expand by an extra 5% on average. Overall the paper estimates excess costs to consumers could range from $2 billion to $20 billion per year, with the most likely number in the middle of that range. That doesn’t mean all of that extra investment is wasted – the capital is still doing something that is presumably useful unless it’s being spent on gold-plated coffee mugs – but it should make regulators think carefully about utilities’ motivations when they argue for particular new capital expenditures.

Obviously, we need electric utilities, and we even need gas utilities for at least a while. Some people may argue K&S’s results make the case for government-owned utilities so there are no shareholders to compensate, but to anyone who has studied the alternatives carefully, it’s clear that each model is subject to abundant inefficiencies. I think this study should be another reminder not just that regulating utilities is a tough job, but also that investing in high-quality regulation – hiring adequate numbers of highly-skilled staff, paying well enough to retain the best of them, and giving them the resources to do their jobs – is likely to have enormous payback.

Find me @BorensteinS most days tweeting energy news/research/blogs.

Keep up with Energy Institute blog posts, research, and events on Twitter @energyathaas.

Suggested citation: Borenstein, Severin, “What Does Capital Really Cost a Utility?” Energy Institute Blog, UC Berkeley, October 3, 2022, https://energyathaas.wordpress.com/2022/10/03/what-does-capital-really-cost-a-utility/

Categories

Severin Borenstein View All

Severin Borenstein is Professor of the Graduate School in the Economic Analysis and Policy Group at the Haas School of Business and Faculty Director of the Energy Institute at Haas. He received his A.B. from U.C. Berkeley and Ph.D. in Economics from M.I.T. His research focuses on the economics of renewable energy, economic policies for reducing greenhouse gases, and alternative models of retail electricity pricing. Borenstein is also a research associate of the National Bureau of Economic Research in Cambridge, MA. He served on the Board of Governors of the California Power Exchange from 1997 to 2003. During 1999-2000, he was a member of the California Attorney General's Gasoline Price Task Force. In 2012-13, he served on the Emissions Market Assessment Committee, which advised the California Air Resources Board on the operation of California’s Cap and Trade market for greenhouse gases. In 2014, he was appointed to the California Energy Commission’s Petroleum Market Advisory Committee, which he chaired from 2015 until the Committee was dissolved in 2017. From 2015-2020, he served on the Advisory Council of the Bay Area Air Quality Management District. Since 2019, he has been a member of the Governing Board of the California Independent System Operator.

This phenomenon is not limited to state regulatory commissions. The Federal Energy Regulatory Commission sets authorized ROEs for transmission and generation assets in wholesale rate bases, and has relied on wild hand-waving arguments for decades about how risky those assets are and how dysfunctional U.S. capital markets have been since the Great Recession, both justifying higher ROEs that also do not track capital markets generally. The upward bias or equity premium at the federal level must be added to the bias at the state level in order to estimate the total effect on consumers, and the Averch-Johnson effect is reflected in the ambitious plans to build high-voltage transmission lines, the costs of which are not subject to competitive forces, ex ante review by the Commission, or ex post prudence review. There is essentially no regulatory oversight of the cost or prudence of these wholesale facilities, but instead a clear directive that more transmission capacity is always a good thing. I hope that someone will take on the federal version of this problem.

Thank you for posting this paper. I was clued into an earlier version in this blog and I used that to support my testimony before the CPUC on setting rate of return. These two blog posts summarized my own findings for the three large California utilities in 2019 which is consistent with the paper here.

https://mcubedecon.com/2019/11/12/utilities-returns-are-too-high-part-1/

https://mcubedecon.com/2019/11/13/utilities-returns-are-too-high-part-2/

As it stands today, Sempra and Edison International are worth about twice what the CPUC has authorized in book value. (PG&E, despite emerging from bankruptcy, is at book value.) In other words, ratepayers will pay twice for capital investment what they were told they would have to pay. And ratepayers have not benefited from the fall in cost of capital over the last 40 years. Last fall the utilities fought a mandated decrease in their returns on equity (ROE) due to falling bond rates, illustrating this paper’s finding about downward stickiness on ROEs.

One point: CAPM is not an empirically valid measure of costs of capital. Fama & French (2004) (cited nearly 800 times so far) found that while it has a nice neat theoretical foundation, it hasn’t worked out in the data. There have been some recent new formulations, but those have not yet been widely adopted. The single biggest problem is the definition and calculation of the “market rate premium” at the core of the calculation. The endogenous nature creates a reinforcing feedback loop that makes the rate insensitive to changing market conditions.

We need a new method for setting the ROE that isn’t so reliant on the finance theory that led to the 1998 and 2008 market crashes.

Such a timely study! Thank you Borenstein and team.

The K&S chart says it all. If real world companies cannot obtain returns which are comparable to what utilities are awarded by group of commissioners, don’t expect the utilities to pay attention to the real world. With so many new technologies for generation, management, and conservation in providing electricity, we need our policies to keep up. Setting the right rate of return and understanding the cost of capital is critical to providing the incentive structure needed to have our utilities and their shareholders motivated to make good decisions and not rely on preserving a high rate of return while stuck favoring old practices and technologies. Energy cost and reliability has been a determinant of a country’s economic might for centuries and the USA should not let our energy systems become inefficient.

I look forward to more great studies from The Haas School of Business and our other great educational and financial institutions in this country.

This study is very timely and I’m so glad the Borenstein team spent the time and resources to study such a complex, but important issue. The cost and availability of energy as a basic economic input has generally defined the wealth of countries for centuries. The new technologies and tools need policies to keep up and this study shows a large gap between what all other industries in the real world can achieve versus what our nations Regulatory Commissions are awarding utilities. With a growing gap over time (the K&S chart in the study) plus the growing use of fees, riders, and tariffs that pay for risks normal business must absorb indicates our system is hurting efficiency and productivity. Worse, the overly high rates of return awarded by a group of people makes real world options financially unattractive to entertain leaving us with a system which adapts to changes slowly and keeps costs high. With the macro-economic dynamics of adjusting global supply chains, the USA must align regulated monopolies to have a capital cost similar to the real world so common-sense decisions are made because motivations and incentives match the real world.

I look forward to more information on this and similar topics from The Haas School of Business and the other great educational and financial institutions we have in this country.

Indeed utilities have been awarded excessive allowances for the cost of capital.

The Capital Asset Pricing Model (CAPM) fell into disfavor with regulators for a variety of reasons, and has been displaced by the Comparable Earnings method, the Discounted Cash Flow (DCF) method, and the Equity Risk Premium method.

Utilities generally prefer the Comparable Earnings method, which simply looks at what other companies are getting, a circular analysis that never looks at fundamentals of the market.

I tend to prefer the Equity Risk Premium method, illustrated by the graphic above that shows allowed ROE for utilities having a bigger and bigger advantage over returns on government and corporate bonds over the past couple of decades — bond rates had declined, and utility allowed returns had not. In essence, “regulatory lag” created a windfall for utility investors.

But now we are entering into a period of higher interest rates. Regulators have the option to ALSO be slow to adapt to higher interest rates. By doing so, they can allow the historical relationship between utility allowed returns and the cost of capital to be restored.

It’s nice to see Haas talking about revenue requirement for a change. Past blogs have proposed redistributing the cost burden of the utility revenue between customer groups — higher charges to customers with investments in energy efficiency and renewable energy, lower charges to customers who use large amounts of electricity.

Cutting the allowed return to a fair rate, and eliminating the inclusion of excessive corporate executive compensation from rates will do a lot to address the perceived challenges to electrification.

I look forward to a future blog, comparing the executive compensation for utilities to the compensation levels for public sector workers in State Government who do jobs with comparable levels of responsibility and comparable numbers of employees supervised. The CEO of PG&E is paid about $40 million/year; the Governor of California (who supervises a MUCH larger enterprise) is paid less than 1% of that amount.

So we now have two compelling reasons to overhaul the utilities’ rate structure, taxes/programs that really should be part of the State’s general budget and outsized returns on [unnecessary] investments.

I am uncertain of this, but wouldn’t the parent companies of these wholly owned subsidiaries benefit twice from these inequities?